Why working from home hurts the high street

Although restrictions on opening are being lifted, high street businesses remain at risk while office workers remain at home.

Although restrictions on opening are being lifted, high street businesses remain at risk while office workers remain at home.

Now the economy is opening back up again after lockdown, it is tempting to think that high streets are returning to normal. But assuming this misses a critical piece for vibrant high streets and city centres – office workers spending money in shops, restaurants and pubs close to where they work.

Before the lockdown, strong city centres with lots of higher skilled office jobs also had the fewest high street vacancies. Places like Bristol and Manchester, where offices take up over half of the commercial city centre floorspace, had fewer empty shops on the high street so the amenities that were available were more plentiful and more premium.

This is because the office jobs bring in hundreds and thousands of higher paid people with spare cash in their pockets into the city centre every day. These people might pick up a coffee on the way to their desk, pop into a shop in their lunch hour or grab a pint at the pub after work. This means that a business in a place like Cardiff is putting money into its tills Monday to Friday and is far less reliant on weekend trade to keep it afloat, compared to one in say, Swansea or Newport.

This relationship has somewhat turned on its head since the lockdown. Given their relative ease of working from home, office jobs were the first to move out of the city centres and will be the last to come back, and this has hit the strongest city centres the hardest.

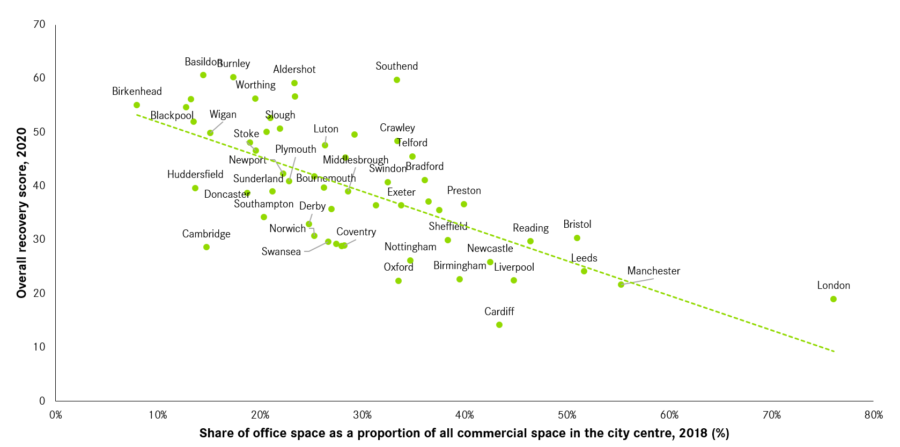

Figure 1 plots the share of office space in each city centre against the overall recovery score (relative to pre-lockdown levels) for that city centre, as of the penultimate calendar week of June.

As the scatter and the line of best fit suggest, there is a negative relationship between the two. City centres like Liverpool and London with a greater focus on offices lag further in their return to ‘normal’ levels of activity than those like neighbouring Birkenhead and Basildon respectively where office jobs are not so central to the city centre economy.

Liverpool city centre has 45 per cent of its commercial floorspace dedicated to offices and has around 16 per cent of the footfall as it used to before the lockdown. Birkenhead on the other hand, has only 8 per cent of its space for offices and its footfall has recovered to nearly 45 per cent of what it used to be.

Figure 1: Share of office space vs. Overall score to recovery across GB city centres

Source: Valuation Office Agency, 2018. Locomizer, 2020

Even though the shops are open, and the venues will be able to serve food and drink soon, the core customer base in city centres, especially the strong ones, is still and will, for a while to come, be missing.

This of course, has a huge impact on viability of these businesses, especially as furlough starts to be tapered. We need to look no further than Pret for a classic case – the café chain announced earlier this week that sales remain low and that they are considering cutting jobs.

These circumstances call for a data-driven and responsive approach to our high streets and their recovery, as outlined in our recovery framework.

Tools such as the High Streets Recovery Tracker should be used to understand, in near real-time, whether allowing the supply-side of retail and leisure to resume operations is enough to attract people and increase activity on the high streets. There are three possible scenarios:

The idea of retail and leisure facilities reopening is a welcome respite after months of lockdown for a lot of places. Our strongest city centres, however, will need to wait a little while longer before office workers are allowed to come back and a sense of ‘normal’ returns. Only time will tell whether the experience of lockdown will tweak or transform our working practices. Either way, the follow-on impact on the high streets cannot and should not be ignored.

Leave a comment

Be the first to add a comment.