02Exporters play an important role in the national economy

Exporters, businesses that trade services and goods in Britain and overseas, account for over five million jobs in the UK economy. While exporters account for a smaller share of businesses and jobs compared to the local services sector (25 per cent of employment compared to 75 per cent in local services), exporters play an important role in the UK economy for several reasons:

- Firstly, they tend to be more productive than local services businesses – and also drive productivity growth, which drives long-run economic growth.

- Secondly, because exporters generate their revenues from selling into wider domestic and international markets, they generate income independent of the performance of the local economy.5

- Thirdly, businesses in the export base have a multiplier effect on jobs in local services but the size of the multiplier varies according to the type of exporting business. Cities that have more exporting jobs also have more jobs in local services, relative to the size of the working-age population but the relationship between high skill exporting jobs and local services jobs is stronger and suggests that high-skill exporters create even higher demand for local services.

It is for these reasons that the industrial strategy should focus on growing Britain’s export base if its strategic objective is to promote economic growth and boost productivity.

The skills profile of exporters is more important than the sectoral profile for boosting productivity in cities

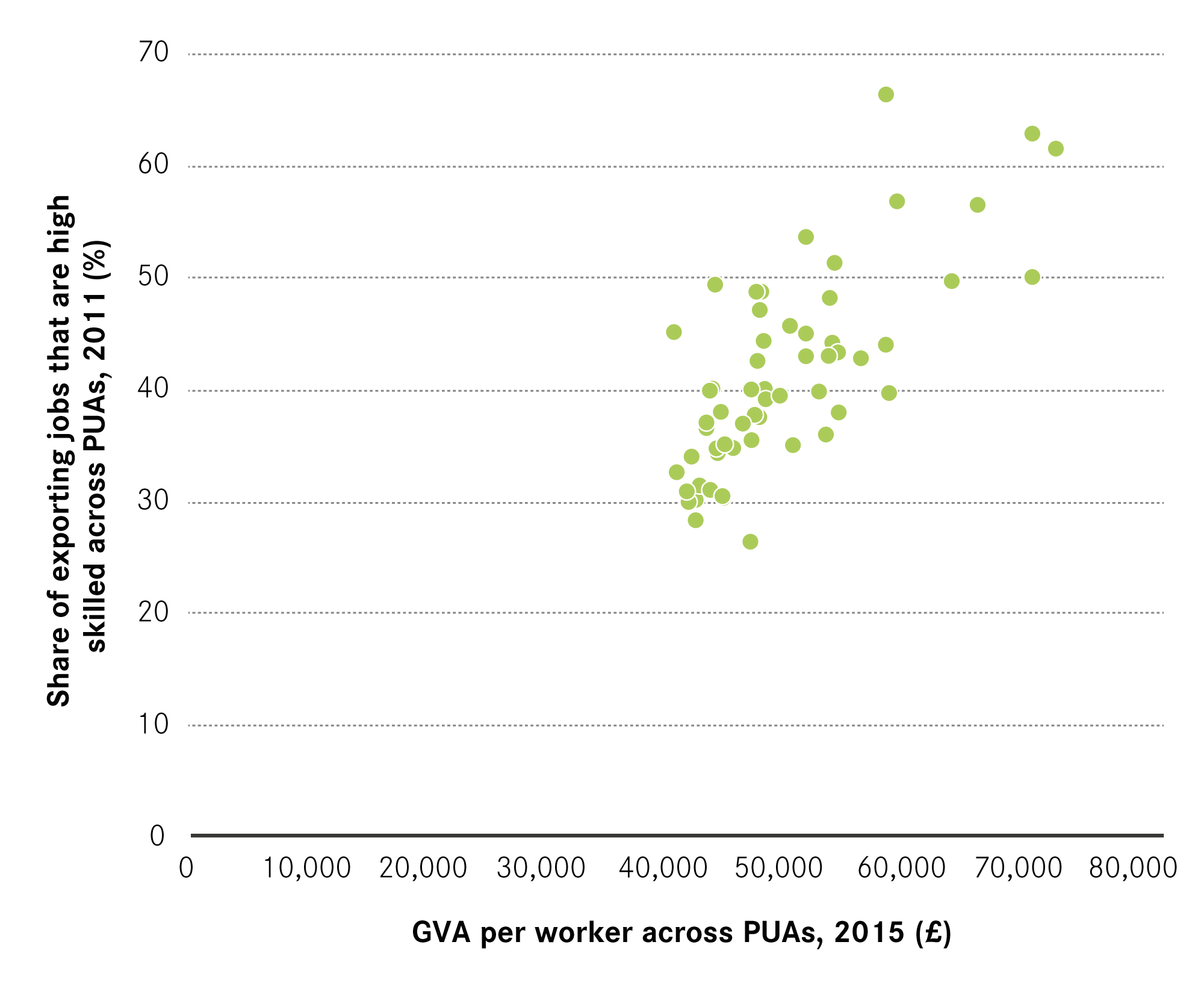

Having a large number of exporters does not necessarily mean a city is more productive, however – it is the nature of the export base that matters. Some cities have a large export base but are less productive: 35 per cent of jobs in Sunderland are in exporting firms 1.6 times the national average, but productivity (as measured by GVA per worker) is less than 90 per cent of the national average. In particular, cities that tend to have a larger proportion of their export-base jobs in the service-exporting sector are on average more productive than cities that tend to have a larger proportion of goods-exporting jobs (see Figure 1)

Figure 1: Relationship between productivity and the sectoral profile of exporting sector in cities

Figure 2: Relationship between productivity and the skill profile of exporting jobs in cities

The relationship between levels of productivity and the skills profile of the export base is stronger than the sectoral profile of the export base (see Figure 2). While services exporters tend to be high knowledge on average, the findings suggest that the skills profile of the export base – encompassing services and goods exporters – has a more important bearing on the economic performance of cities than the sectoral profile.6 This suggests that focusing on the factors that support the growth of these types of businesses is likely to be more important that sector-specific policies.

High-skilled exporting activities – those that are more intensive in communication and cognitive skills – are also at lower risk of being off-shored or automated compared to medium-skilled exporting activities.7

High skilled exporters are not evenly or randomly located across the UK

High-skilled exporters are particularly likely to concentrate in cities because of the benefits that are derived from co-location.

Exporters tend to cluster in cities because of the benefits that density and proximity bring – the returns to agglomeration. Agglomeration is the process by which concentrating economic activity in one place makes businesses and workers more productive.

There are three main mechanisms through which the benefits that businesses and workers derive from locating in close proximity to one another are generated:

- Learning: the ability to exchange ideas and information, known as ‘knowledge spillovers’. Knowledge flows between firms occur through social interaction and in proximity to a knowledge source.8 This suggests that knowledge spillovers best operate over small and dense geographies, where new knowledge is created.9

- Matching: the ability to recruit from a deep pool of workers with relevant skills. Larger markets – such as those in cities – imply more jobs and deeper pool of workers. Access to larger and more stable labour market and qualified pool of workers is important: businesses can more easily be matched to workers with specialised skills and this lowers the probability of labour shortage.

- Sharing: the ability to share inputs, supply chains and infrastructure. Larger markets allows for a more efficient sharing of local infrastructure and facilities, and offer producers the advantages of access to a larger variety of intermediate input suppliers.10

The benefits businesses derive from being in close proximity to other businesses helps explain why British cities are home to 52 per cent of all businesses and 59 per cent of all jobs – despite covering just 9 per cent of land across the country. But the returns to co-location are higher for some types of firms meaning that some firms are more likely to locate in urban locations and this is true of exporters.

54 per cent of exporters and 65 per cent of high-knowledge exporters locate in cities.

The export base varies across different cities

The size and nature of the export base in a city is driven in part by the place-based characteristics that cities offer different types of firms.

Businesses benefit from locating in cities whether they are located in city centres or suburbs but in different ways. High-skilled and knowledge-focused exporters tend to favour city-centre locations because city centres tend to be denser, which facilitates the exchange of knowledge and ideas.

Cities also offer important benefits to lower-skilled and more-routinised businesses but because access to knowledge and ideas are less important they are less likely to locate in dense city centres and are much more likely to be found in suburbs.

But city centres and suburbs do not play the same role in all cities which has an important bearing on the geography of exporters more generally.

This section examines the size and the skill profile of exporters across city centres and suburbs of different cities.

Box 2: Defining city centres and suburbs

The analysis in this report makes a distinction between two parts of a city: city centres and suburbs.

City centres are defined based on all the postcodes that fall within a circle from the pre-defined city centre point. The radius of the circle depends on the size of the residential population of a city and its size is as follows:

- London – radius of 2 miles

- Large cities – radius of 0.8 miles

- Medium and small cities – radius of 0.5 miles.

Suburbs are defined based on the postcodes that fall within the rest of a city (defined as primary urban areas (PUAs), the standard definition of cities that Centre for Cities uses). In some areas, the suburbs will include towns, such as Oldham in Manchester.

City centres with a large proportion of exporters also tend to have a more highly-skilled export base.

Across all city centres, there is a positive relationship between the size of the export base and the skill profile of exporting jobs (see Figure 3). For example, in Milton Keynes its city centre is home to nearly 30 per cent of the city’s export jobs, and 58 per cent of those jobs are high skilled. The proportion of export jobs in London’s city centre is 26 per cent, well above the city centre average of 15 percent and over three quarters of those jobs are high skilled, much higher than the city centre average of 46 per cent.

In contrast, city centres with small export bases tend to have lower-skilled export bases. Less than 5 per cent of jobs in Blackpool city centre and 7 per cent in Doncaster city centre are in the exporting firms and less than a third of these jobs in both cities are high skilled, over a third less than the city centre average.

Figure 3: Relationship between the size of the export base and the skill profile of exporting jobs in city centres

Some city centres have a relatively small, high-knowledge export base. City centres in this category included Aldershot, Cambridge, Coventry, Exeter, Liverpool, Newcastle, Nottingham, Plymouth, Southampton, Worthing and York. In Cambridge and York in particular, their historic city centres have tended to constrain city centre development, which means that high skilled exporting businesses tend to locate in their suburbs.11

Only a handful of city centres have a large, low-knowledge export base, and these include Blackburn, Bradford, Huddersfield, Ipswich and Portsmouth. The export base in these city centres includes a relatively high concentration of manufacturing exporters which suggests that agglomeration economies do not play out in the same way in these city centres as they do elsewhere.

The larger the export base in a suburb, the lower skilled those jobs tend to be

Overall, the relationship between the size of export base and the skill profile of exporting jobs is negative in the suburbs (see Figure 4) – this is in contrast to the relationship found across the city centres.

The suburbs of Burnley had one of the highest concentrations of export jobs – 39 per cent of jobs were in the exporting firms, 12 percentage points higher than the city average. But less than a third of these jobs were high skilled, compared to 40 per cent across city suburbs as a whole. Similarly, in Sunderland 38 per cent of jobs in the city’s suburbs were in the exporting businesses but just 26 per cent were high skilled.

In contrast, just 18 per cent of jobs in London’s suburbs were in the exporting firms but more than half (54 per cent) of those jobs were high skilled. The proportion of jobs in the exporting firms in Exeter’s suburbs was also low, less than 17 per cent, but nearly half of those jobs also tended to be high skilled (49 per cent).

Figure 4: Relationship between the size of the export base and the skill profile of exporting jobs in suburbs

The export base in the suburbs of Aldershot, Cambridge and Reading were large and highly skilled. A far larger proportion of jobs in Cambridge’s suburbs were in the exporting firms, 28 per cent, compared to its city centre, and two in three of those jobs (67 per cent) were high skilled. Data shows that all three cities had a relatively high concentration of R&D activity. This type of activity tends to be high skilled and concentrated in suburbs (see the Cambridge case study).12