01Introduction

Attracting capital investment – for example in business premises and infrastructure – is a crucial part of urban economic development. High quality facilities, efficient infrastructure and well-designed places are an important part of attracting new businesses and creating new jobs. And in the context of the devolution of business rates, securing this investment is becoming ever more important for cities.1

The private sector plays a vital role in delivering these capital investments, contributing their finance, expertise and entrepreneurial mind-set, and enabling cities to achieve more than is possible for the public sector when it acts alone.2 Successful private sector-led development is a catalyst for further investment, demonstrating the competitiveness of the city to others in the industry. So cities across the UK are continually seeking investment, to both stimulate and maintain their economic growth.

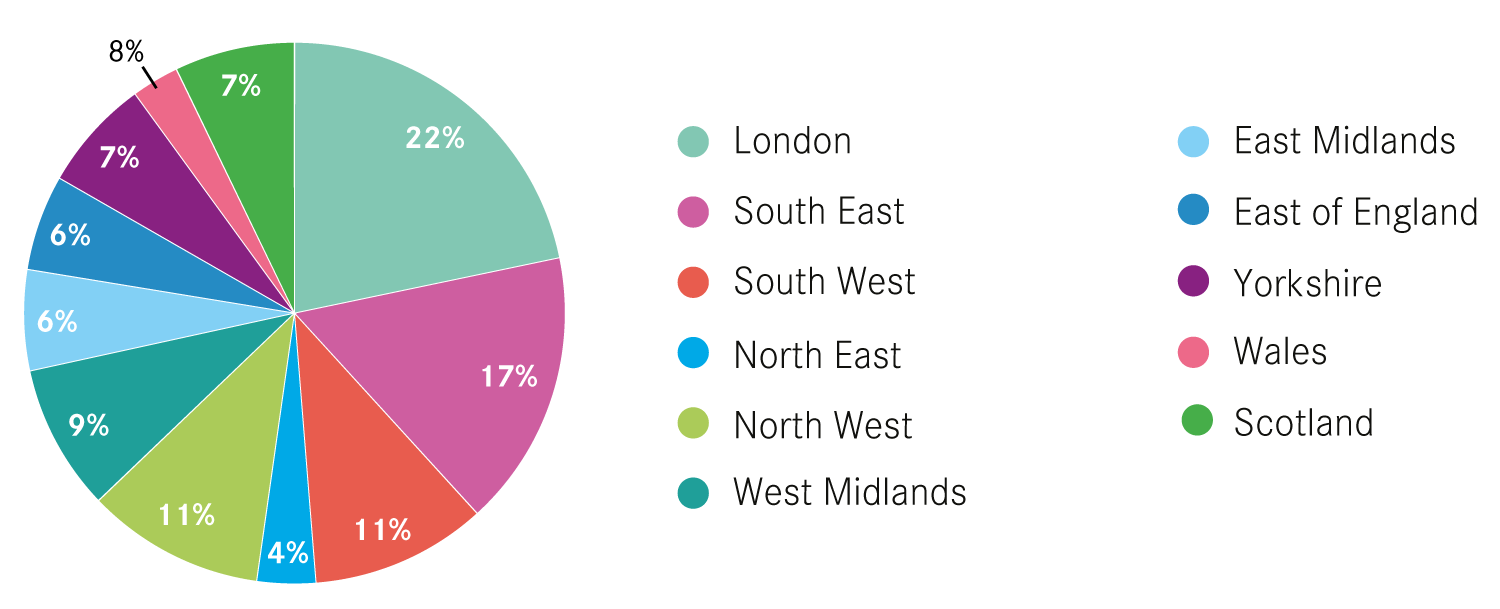

Some cities have been more successful than others at attracting this investment in recent years. London dominates commercial property investment in Britain (unsurprising given the scale of London and its standing as a leading global city). As Figure 1 shows, half of the UK’s commercial property investment was in the capital in 2016, whilst the South East attracted over 10 per cent. Other regions were less prominent, collectively accounting for just over a third of total investment.

When measured by the number of transactions the figures are much more evenly spread, as shown in Figure 2. This is to a large extent due to high property prices in the capital – investments outside London are on average of a smaller value. For example, while Yorkshire accounted for just 3 per cent of the total value of investment in 2016, 7 per cent of transactions took place in the region.

Figure 1: Regional shares of commercial property investment volumes, 2016

Figure 2: Regional shares of commercial property investment transactions, 2016

London’s large investments occur in spite of better yields being available elsewhere in the country. This is in part due to the make-up of investors and their differing priorities. The London market is heavily dominated by overseas investors who seek to diversify outside their own economies, secure prestigious assets or make foreign currency gains and so are drawn to the capital.4 5 6 For domestic investors the return is the priority, so regional cities, and the higher yields they offer, are an increasingly attractive option.7 In 2016, the average commercial property yield – a measure of the annual income return to an investment – was 6.3 per cent in the North West and 6.7 per cent in Wales, compared with 4.4 per cent in London.8

There are clear opportunities for investors outside of London. What is less clear is the role that the cities themselves have to play in attracting this investment.

This report provides a guide to what investors are looking for when making an investment, and makes a series of practical recommendations for cities to improve their approach to attracting investment. The findings and recommendations are based on interviews with investors, developers, real estate professionals and cities themselves and a review of the existing literature.

The first section of the report explores what attracts private sector investors to cities, providing cities with an insight into how investors choose their investment locations and which city characteristics and behaviours they prioritise. A strong understanding of this is the best foundation on which to develop a city’s approach to attracting investment.

The second section of the report develops this insight into a guide for cities, providing practical advice on how best to attract investment. While having strong characteristics is only part of the equation, knowing the industry personally and having a high profile and positive reputation is also crucial for securing investment.

Box 1: Defining private sector investment

In this report we define investment as capital investment – investment in, or development of, a city’s buildings and infrastructure. It does not refer to business investment – businesses choosing to locate in a city. These businesses are the occupiers, and users, of the capital investment. This report also focuses on investment by the private sector, rather than the public sector.

For the most part, the research refers to real estate investment and development. Real estate generally includes retail, offices, industrial and residential properties, as well as alternatives such as hotels, healthcare facilities and car parks. Development tends to be higher risk and shorter term than investment in existing buildings.

Although the report mostly discusses real estate investment, the findings and recommendations are also applicable to infrastructure investment (in roads, bridges and utilities, for example). Private sector investments in infrastructure tend to be less volatile than real estate and much longer-term.