02The economic importance of city centres

We know that UK city economies are at the heart of the national economy: they are 21 per cent more productive than non-urban areas and host 72 per cent of all highly skilled jobs. But the particularly important role of city centres to UK city economies, and the national economy overall, is often left out of policy discussions. In fact, the strongest performing city centres are the most productive parts of the UK economy, and host more productive and higher paying jobs than other areas of UK cities.

On average, almost a quarter of all private sector jobs in cities are now based in their centres. And around 9 per cent of jobs in the UK are located in the city centres of the 10 largest cities, despite these areas accounting for just 0.03 per cent2 of all land in the UK. Businesses will often pay a premium to be based in one of these city centre locations because of the benefits they bring.

City centres and the benefits of agglomeration

The primary gain for business of locating in a city centre is proximity, or agglomeration, and this offers three main benefits to businesses locating in city centres. These are:

- The ability to share inputs and infrastructure, such as roads, rail and street lights

- The ability to recruit from a deep pool of workers with relevant skills

- The ability to exchange ideas and information, known as ‘knowledge spillovers’

While the first two benefits operate over a city wide level – a business based on a business park has access to the same potential recruits as a city centre business – the third operates over a much smaller geographic area.3 It is this third factor which is so important to the services-based knowledge economy: knowledge is best spread via face-to-face interactions and these face-to-face interactions are more likely to occur over much smaller distances in more dense areas, where both formal and informal meetings are more likely to come about. Within a city, this area is the city centre.

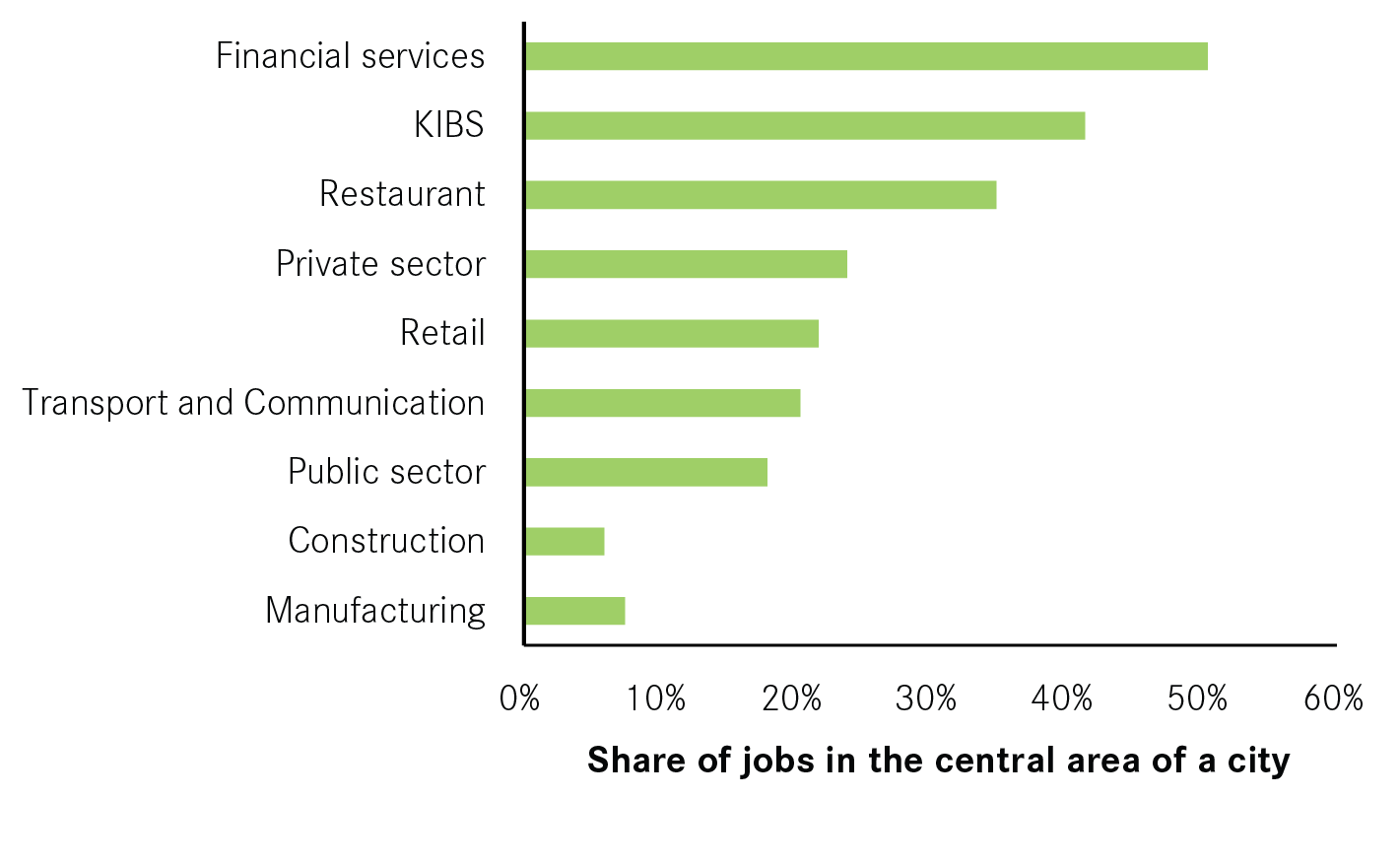

Of course, not all businesses prefer city centre locations. As figure 1 illustrates, of all the manufacturing and construction jobs in cities, just 6 and 7 per cent of these jobs respectively are located in or close to city centres. This is because these types of activities require cheap land and good transport links more than they require access to knowledge and information.

Figure 1: Concentration of jobs in the central areas of cities, 2011

In a services-based economy, knowledge intensive business services (KIBS) benefit the most from agglomeration effects and knowledge spillovers. Whereas around 24 per cent of private sector jobs in cities are located in or around city centres, this figure is 41 per cent of KIBS jobs. The figure is even higher for financial services jobs – a subset of KIBS jobs – one in two of which are based in city centres, and because of global competitive pressures, the UK is very likely to continue to specialise in knowledge-intensive activities.

This trend is also likely to persist despite advances in communications technologies that have supposedly resulted in the ‘death of distance’ which reduce the need for physical proximity in knowledge-intensive sectors. Yet, innovations such as email and video conferencing have neither led to a rise in home working nor have they rendered proximity irrelevant. This is because it is face-to-face interaction that primarily facilitates the spread of knowledge.

First order impact of the city centre economy: sustainable employment and job quality

If cities want to improve the number and quality of jobs available, they need to focus on creating city centres that function well as locations that attract businesses. The density and proximity that city centres offer are attractive to businesses for a number of reasons, so the first aim in making a city centre a more attractive business location should be to increase the economic scale of the city centre, concentrating all types of office based business there.

The national economy is increasingly specialising towards knowledge-based jobs that gain most from agglomeration, so city centres are likely to become increasingly important in the future. KIBS jobs are twice as likely to be concentrated in city centres and these types of jobs offer higher wages and more career opportunities to workers. 50 per cent of the jobs in city centres tend to be taken by graduates, as opposed 33 per cent for all other parts of England and Wales, illustrating the attraction that city centres hold for knowledge-based businesses and jobs.4 Cities without KIBS jobs on the other hand, tend to have a higher proportion of jobs available in lower paid, less secure jobs, which risk creating cycles of workers stuck in low-pay, causing knock-on impacts for firm profits and economic output of the city overall.

Second order impacts of the city centre economy

Alongside creating attractive places to do business, focusing on revitalising the centres in cities of all sizes is also important; this can drive growth and improve the following:

Access to jobs

A thriving city centre can be attractive to job-creating private sector businesses and growth. The knock-on effects of this are that city centres need effective public transport, ensuring workers can access these jobs. Lower income groups in particular are more dependent on public transport – 43 per cent of people living in households in the lowest real income group have no access to a car or van compared to 8 per cent of people living in households in the highest real income group. Over two thirds of Jobseekers Allowance claimants have no access to their own car or cannot drive.

Good public transport systems which link people to jobs and essential services are key to supporting economic growth. Densely populated city centres make delivering this public transport cheaper and more effective.

Environment and public realm

Thriving city centres, which include businesses located close together, retail and entertainment close by, along with residential areas, result in less sprawl. A more dispersed city economy, however, generally increases the requirement for private transport, as providing good public transport links to a number of employment sites become more expensive. This has implications for CO2 emissions and the environmental sustainability of a city.

The top 10 cities that have the lowest road transport CO2 emissions had on average 27 per cent of all jobs in their central areas in 2011, while the 10 cities with the highest emissions on average had 17 per cent of all jobs located in their central areas. It is not enough, however, to have economic activity centralised to reduce CO2 emissions, growth must be supported by an efficient public transport system. This also underlines that when considering a city centre economy, local and central government must not only think about specific development sites, but about access to them – transport links to and from the city centre are an important component of central economies.

Retail and the high street

Past and current government policy towards city centres has narrowly focused on the performance of the high street. But retail is a secondary activity that feeds off the primary activities of a city centre economy.

Umployment in particular pulls people in to city centres, increasing footfall, creating a market for retailers and restaurants to sell to. Those cities with strong city centre economies tend to have a strongly performing high street, while those cities with a more dispersed economy have lower footfall in their city centres, their high streets then struggle as a result.

Box 1: The changing role of city centres in UK cities over time

At the start of the industrial revolution, the manufacturing firms that drove the national economy, and established many UK cities as industrial powerhouses, tended to located close together around key transport and infrastructure nodes such as ports and coalfields, minimising expenditure on expensive fuel. The advent and increased availability of electricity, however, as well as falling transport costs, encouraged manufacturers to move further apart from each other, spreading out across and beyond cities, to capitalise on cheaper land. Economic growth was heavily dependent on the production and trade of goods, where the city centre’s economic role was relatively less important than it is today.

Today the UK economy is no longer primarily manufacturing-led and in the decades since 1970, industry-led growth has declined as a proportion of national economic output. The service sector that now dominates the UK economy benefits from, and requires very different types of, urban ‘amenities’ than heavy industry and manufacturing. Service activities, particularly those that ‘sell’ knowledge, such as finance, law and marketing, benefit from proximity because they benefit from the exchange of ideas that density facilitates.

Insights for city policymakers and practitioners

The performance of city centres across UK cities

Making the most of city centres is vital for all city economies. The overall trend for UK cities since the 1970s has been to decentralise, caused through a combination of more out of town living and labour market changes: 38 out of 63 cities saw a hollowing out of private sector jobs in their central areas in the period before the downturn.

And there appears to be a link between city size and city centre performance. Between 1998 and 2008 larger cities saw their city centres become more important to the city economy: eight of the 10 largest cities saw their city centres become more important, and more than a third of the jobs in large city centres were in knowledge-intensive sectors. Smaller cities, however, experienced the reverse trend, with private sector jobs, and knowledge-intensive jobs in particular, moving away from the city centre.

There are some exceptions to this trend, however. Over the period 1998-2008, Brighton, Reading and Milton Keynes all saw jobs concentrate in their city centres. This suggests that the benefits of agglomeration are not just generated in large cities, nor do large cities have denser cores than smaller cities.

Overall though, the economic downturn has further cemented the trend, with large cities seeing virtually no change in the share of private sector jobs across their economies, and smaller and medium-sized cities seeing a continued decentralisation of private sector jobs. Only London saw a further concentration of its private sector jobs in the period 2008-2011.

Impact of policy to date

City centres are vital for supporting a greater concentration of private sector jobs – and high-value knowledge-intensive jobs in particular – that can gain from the agglomeration benefits that city centres provide. However, some recent government policies have, whether intentionally or unintentionally, actively encouraged out of town patterns of development in UK cities.

Job-focused interventions – inadvertently working against city centres

Out of town Enterprise Zones provide tax incentives and support for businesses to locate in one area, aiming to replicate agglomeration benefits and support growth or concentrating public sector and university locations on certain sites. But out of town Enterprise Zones often displace business from city centres rather than stimulate new growth. This has contributed to the hollowing out of city centres, drawing economic activity away from the city rather than into it. The same logic applies to the subsidisation of out of town business parks – a commonly used policy in economic development in recent years – and the relocation of major public sector employers and universities in out of town locations.

One answer to this – as has been consistently given for retail – is that all out of town development should be stopped. But it is important to note that a city centre location will not be right for every business. So while the public sector should stop subsidising out of town office space, its focus should be on making city centres attractive and viable places to do business and encouraging businesses to locate in them, rather than restricting development elsewhere.

Retail focused interventions – unsuccessfully supporting city centres and the ‘high street’

Policies such as Town Centre First and retail-led regeneration strategies – popular throughout the 1990s and 2000s – have overtly tried to support city centres over out of town locations. But these policies have failed to understand the cause of the underperformance of many high streets.

Sluggish retail is a symptom of a poorly performing city centre economy, not a cause. Those cities that have seen a weakening of their city centre economies pull fewer and fewer workers into their city centres. This reduces footfall, so reducing the market that city centre retailers can sell to. The result is that those cities with strong city centre economies continue to have strongly performing high streets, while those cities with weak city centre economies have also seen their high streets decline in recent years.

If politicians are to ensure cities have strong and vibrant high streets, their aim should be to create policies that strengthen the city centre economy as a whole, rather than focus too narrowly on retail.

Implications and recommendations: making city centres an attractive place for businesses to locate

Thinking about how city centres function as business locations should be the top priority for politicians and policymakers in cities of all sizes. But the interventions required to support city centres are different for cities with weaker city centres, compared to cities with stronger city centres.

Implications for cities with weaker city centres

What is clear for those cities with weak city centres is that these areas are not functioning well as places to do business. The aim of any policy intervention should be to change this.

As set out above, city centres are likely to become increasingly important in the future because of the benefits they bring to high paid, high skilled services jobs. But the first aim in making a city centre a more attractive business location should be to increase the economic scale, attracting any office based business in the first instance.

This would have two main benefits. Firstly, it would concentrate economic activity in one area, allowing the city to get more out of what it already has. Concentrating activity in this way would create demand for retail and other services, make jobs more accessible by public transport and make the city less car dependent. Secondly, a higher level of activity would make it easier to attract higher skilled jobs in the future. It is important to note here however that the ability to attract higher skilled jobs will depend on the number of high skilled workers living in and around a city, so any policies designed to improve a city centre’s appeal to businesses, must also include policies to improve skills.

While cities with weaker centres need to focus on making those areas more attractive to office-based businesses to locate in, they may also want to think about how their city centre can work alongside neighbouring areas. This could include ensuring that public transport services are available to link people and jobs in the city centre and wider labour markets. It might also include improving the residential offer, by raising the quality of the public realm in the city centre making it a more attractive place to live.

Implications for cities with more successful city centres

Those cities with successful city centres need to ensure that the benefits of doing business there (as a result of knowledge spillovers) continue to outweigh the costs of such a location (such as high office rents and congestion). This will include providing effective public transport to tackle congestion and providing sufficient office stock to moderate increases in office rents.

The following section provides examples of types of interventions that politicians and policymakers in cities of all sizes, with weak and strong city centres, should consider to ensure city centres work well as business locations.