03Where are we now: business rates devolution

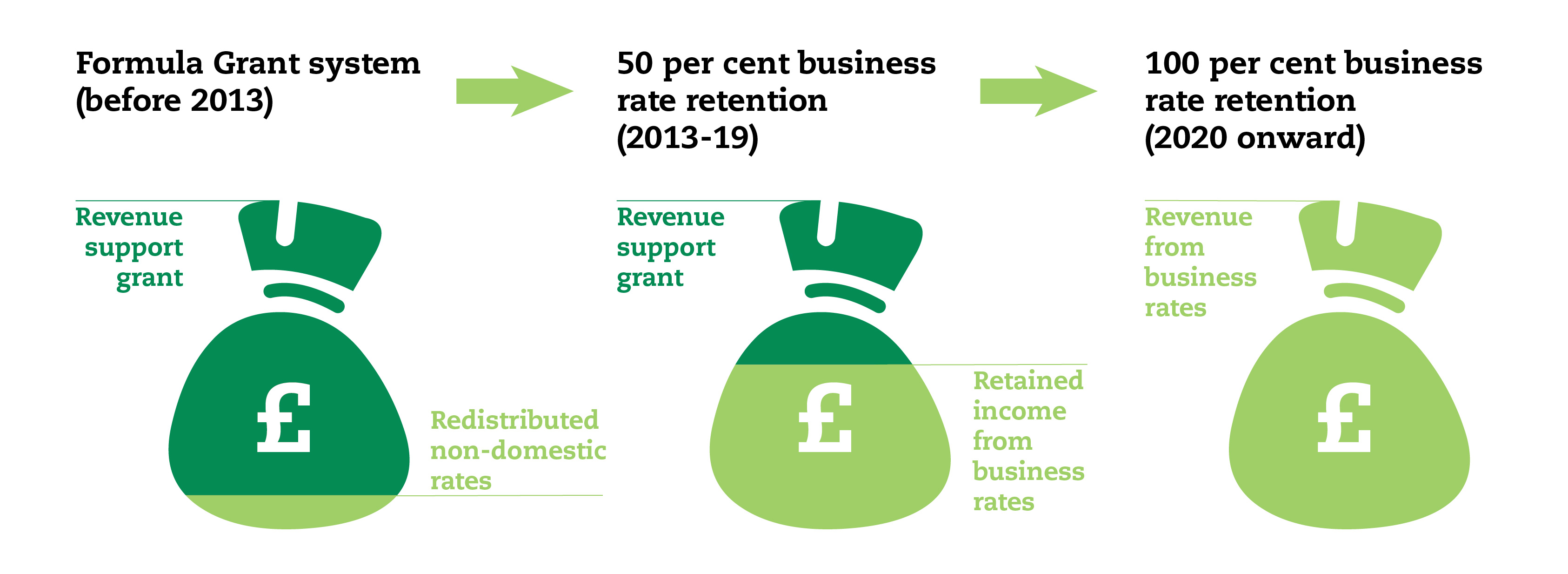

In 2020, business rates will be devolved to local government and will replace the current formula grant funding system. This will give cities greater control over, and an increased reliance on, a growing tax base, which will significantly increase the financial rewards available from supporting economic growth.

How is the system changing?

Business rates, officially known as Non-Domestic Rates, were worth £23 billion in revenues in 2014-15, the equivalent of 14 per cent of the total spent by local government in England.

Typically business rates have funded the formula grant element of the local government funding settlement. Prior to 2013, this was made up primarily of Revenue Support Grant and a small element of redistributed non-domestic rates. The current system, introduced in 2013-14, is made up of a smaller needs-based revenue support grant element and half of business rates revenues. These are are retained by local government and redistributed between local authorities subject to a complex system of top-ups, tariffs and levies.

In 2019-20, the current business rates funded portion of local government funding will be replaced entirely by the total revenue raised from business rates.27 Under the new system, local authorities will be able to reduce the rate at which businesses are taxed and, conditional on having an elected metro mayor in place and subject to a local vote of the LEP, city-regions will be able to raise the rate up to 2 per cent in order to fund infrastructure improvements. If the city-regions that recently agreed devolution deals ahead of the Spending Review had been able to adopt such a precept this year, they could have raised £76 million to spend on infrastructure investments that support local businesses and economic growth.28

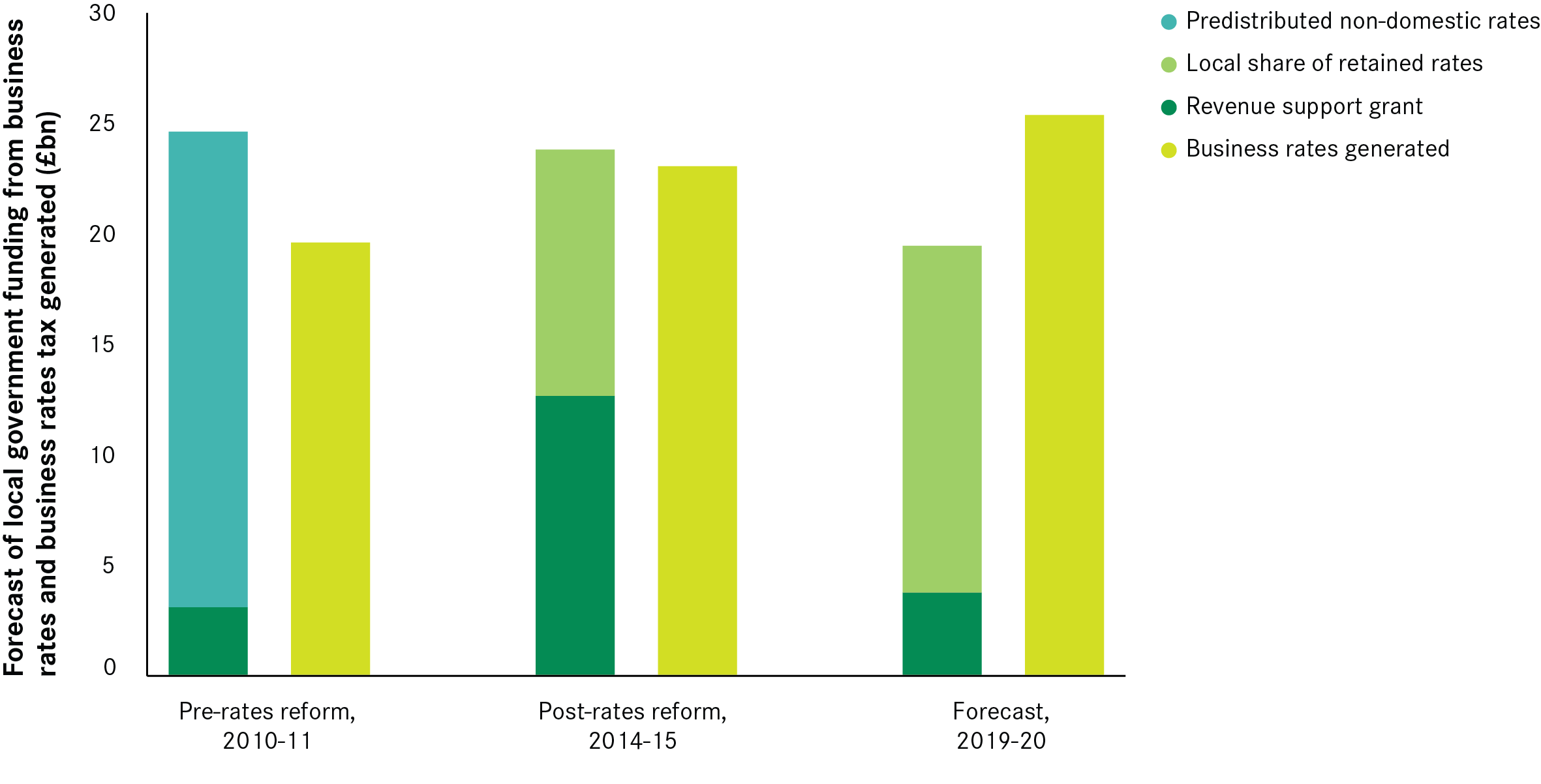

Figure 3: Change in the business rates funded element of the local government funding settlement

Business rates revenues have grown by 18 per cent since 2010-11, while the funding from formula grant has decreased by about 3 per cent over the period. In 2010-11, £5.1 billion more was allocated through formula grant funding than was raised in business rates. In 2014-15, the gap has shrunk to £753 million. Looking ahead to 2019-20, the year in which the new system will be implemented, revenues from business rates are estimated to exceed the combined funding from the local share of business rates and formula grant by £6 billion. In aggregate terms, this means local government will benefit from the devolution of business rates compared to the current system.

Figure 4: Local government funding from business rates and business rates tax generated

What will this look like across local authorities?

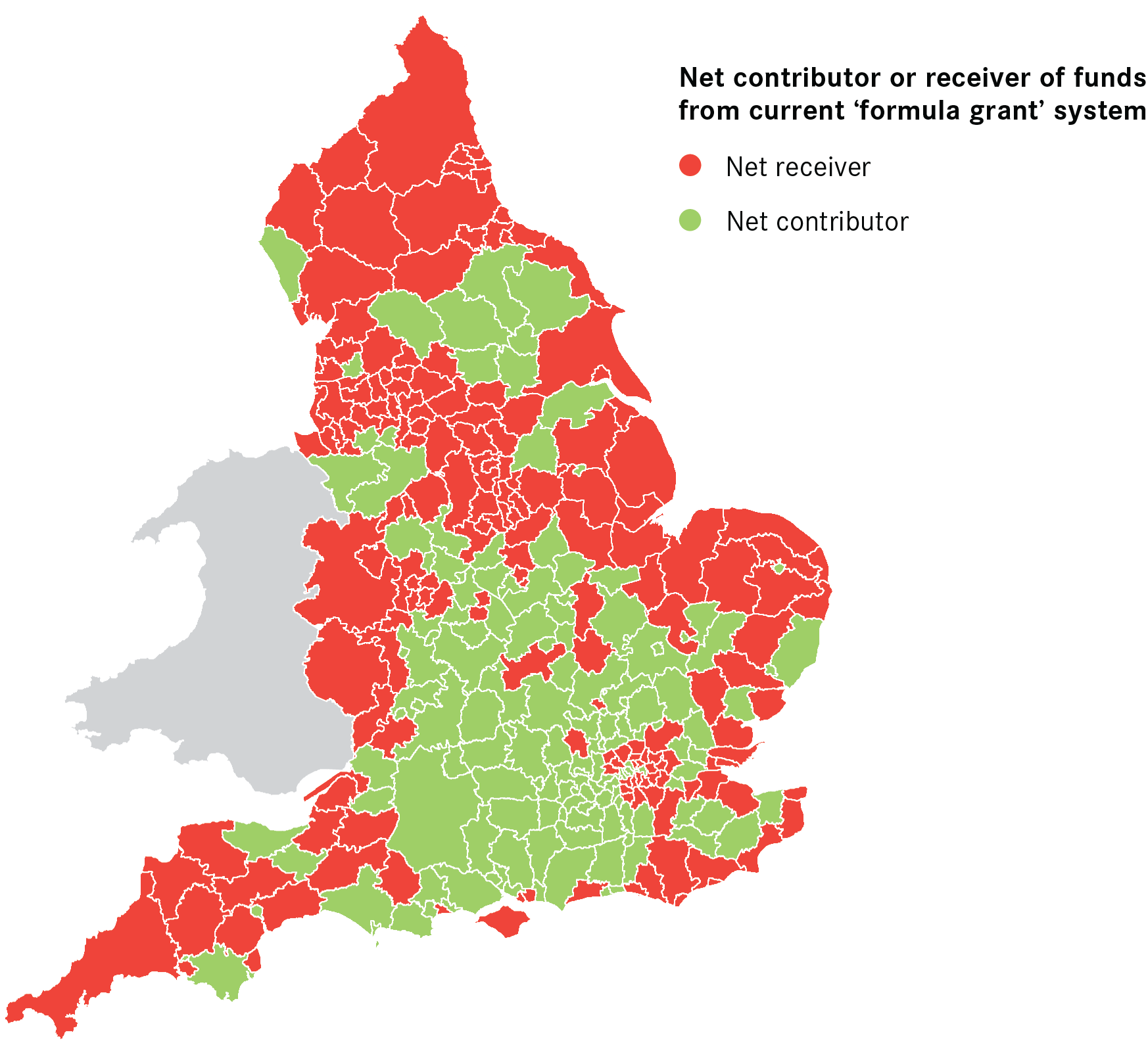

Since the Chancellor’s announcement in October 2015 there has been considerable debate about the likely winners and losers once the amount local authorities have to spend is more closely connected with their ability to generate tax revenues.

Figure 5 shows in which authorities more or less was generated in business rates than was allocated through revenue support grant and redistributed retained rates in 2014-15. In 145 local authorities, more business rates revenue was generated than was received in funding, while the reverse is true in 181 local authorities where less is generated. However, it is important to note that the map of net recievers and contributors to the system does not, and will not, reflect the outcome of the shift to the new funding system.

The new system does not mean that each local authority will simply retain what it raises in business rates locally. Athough the detail of the new system has yet to be announced, the government has been clear that a system of top-ups, tariffs and safety nets will continue to redistribute revenues from those that generate the most to those authorities that generate the least from business rates.

In addition, the majority of local government funding will continue to come from other sources. Together, Revenue Support Grant and the local share of business rates account for 17 per cent of local government spending, which in turn accounts for 20 per cent of total public expenditure in England.

Figure 5: Net contributors and recievers in the ‘formula grant’ system

Improving the current business rates system

With or without greater devolution of business rates, there are long-standing concerns about the design of business rates as a tax and its effectiveness as an incentive for boosting business activity, that need to be addressed in order for the tax to be fit for purpose:

- It is volatile. Five yearly revaluations, or longer if they are delayed, create major shocks to the business rates system for both local government as a revenue stream, and for businesses as ratepayers.

- It is not responsive to economic conditions. The current five-year revaluation cycle also means that businesses are paying rates based on out of-date valuations, which penalises businesses in struggling economies and subsidises businesses in thriving economies. In areas where economic growth has been relatively strong since the recession (and rents have risen), businesses are paying less than they should, based on outdated valuations. By the same logic, in places that have seen rents decrease in the past five years, businesses are paying more than they should.

- It is complex and poorly understood. The mismatch between what the valuation is and businesses’ current ability to pay has created greater need for a broad—and expanding—reliefs programme as evidenced by the new rates reliefs offered in 2010 and extended since. This is both costly to government and a complicated and unpredictable system for businesses and local authorities.

- It can reward perverse behaviour. Because the tax is based on growth in commercial floor-space, the current system rewards space-hungry, often edge or out of town development which can be to the detriment of town and city centres. By the same logic, it does not reward behaviours that support business or economic growth which does not increase net rateable floor space.

To maximise the potential benefits from devolution of business rates the following reforms to the system should be made:

- Replace the fixed yield with a fixed rate. The requirement that business rates should generate a fixed yield in revenue from taxation each year creates distortions in the system which benefit relatively more successful economies. Removing the cap on business rates and moving to a fixed rate system would make business rates a more predictable and efficient tax.

- Conduct more frequent valuations. Properties should be valued every year or, at a minimum, every two years. More frequent valuations and a simpler valuation system would support a more accurate, timely and effective business rates tax system. Frequent valuations maintain the legitimacy of the tax and reduce the risk of sudden, dramatic shifts in tax burdens from large increases in assessed values.

- Extend reset periods. Under the current system baseline funding from the business rates system is set for a five year reset period. There is uncertainty for local authorities at the end of the period, as they do not know how much business rate income will be retained after resetting. Although extending the reset period to a minimum of 10 years would create similar risks towards the end of the longer period, this would provide authorities with longer-term certainty and stability.29

It is worth noting that some argue that the basic principle of a property based business tax is flawed30 and that the current system should be replaced altogether, by a sales tax, for example. The changing business environment, away from floorspace-intensive industrial use, towards more dense land-use in city centres, adds weight to the arguments that a floor-space based property business tax is not fit for purpose.31

Reforming council tax

Alongside business rates reform, there are also changes to council tax that would improve the ability of local government to support growth. Cities need the freedom to raise council tax rates without referendum and to introduce extra council bands in order to better reflect the local economy and distribution of property prices. In the latest Spending Review, the Chancellor announced that local authorities will be able to raise council tax by 2 per cent, in order to help fund social care. The restriction on additional revenues should be lifted, allowing local authorities to spend these funds in ways that best match local needs and priorities.

There are also broader risks and concerns if business rates and council tax are the only game in town when it comes to providing more incentives for cities to support economic growth. The next section looks at why and how we need to go further with fiscal devolution in order to provide stronger incentives for places to support growth and reform public services.