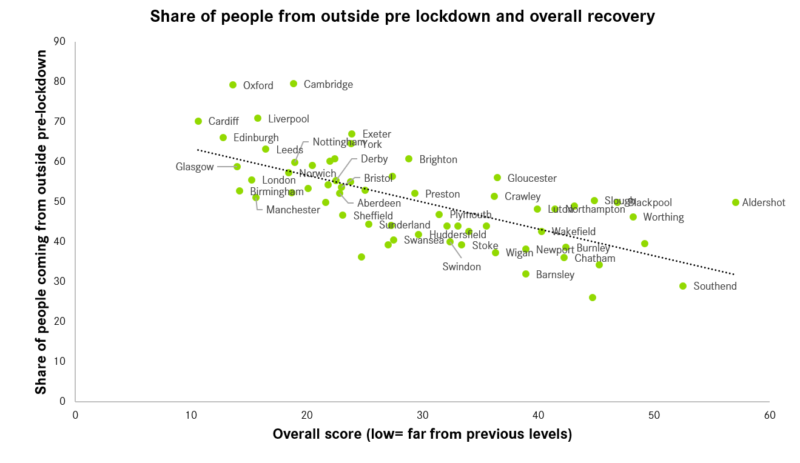

This is likely to be driven by significant reductions in the share of people coming from outside the city

What was a real strength of successful cities before lockdown – their ability to pull people in from far and wide – has now become their Achilles heel in lockdown. As the chart below shows, those places best able to pull people in from beyond their city boundaries are the ones that are also furthest away from a full recovery.

Does this signal a switch from pre-lockdown trends on the relative successes of high streets?

Those previously-successful city centres have a big short-term challenge on their hands – will those visitors and workers that previously flocked to them be both willing and/or able to visit once again? If the answer to this is no then this is bad news for the existing shops, cafés and restaurants that are dependent on their custom, and they will need some short term support.

But in the longer term we know that these city centres have many things going for them, such as high-paid jobs and large resident populations which in turn helped to make their high streets vibrant. In larger and more successful cities, workers in high-skilled exporting jobs who are likely to still be working from home now will probably eventually go back into their city centres and spend their money on local services. When tourism returns, there is little doubt that Oxford, Cambridge or York’s visitors will recreate a market for local businesses and help their high street thrive again.

That less successful places have not seen quite so extreme falls is positive news for their businesses as they look to reopen. But the fundamental reasons for their pre-lockdown struggles have not changed. While a return to ‘normality’ may happen more quickly, it will still require a large, concerted effort from central and local government to turn these city centres around, especially if these places suffer more from the economic hardship which results from the crisis.

More detail can be found on the tracker, which cuts the data according to various aspects of city centre life: workers, weekend visitors, night-time. It will be updated on a monthly basis, plotting the speed of the recovery across city centres, so keep an eye on this space.

Leave a comment

Be the first to add a comment.